Embark on a journey exploring the role of gold as an inflation hedge, delving into its historical performance and why it’s a preferred choice in times of economic uncertainty.

Discover the intricate relationship between inflation rates and the value of gold, offering a unique perspective on wealth protection.

Gold as an Inflation Hedge

Gold has long been considered a reliable hedge against inflation due to its historical performance during times of economic uncertainty and rising prices.

Historical Performance

During periods of high inflation, gold has often shown an inverse relationship with the value of fiat currencies. This means that as inflation rises, the price of gold tends to increase, preserving the purchasing power of investors.

Factors Making Gold Popular

- Scarcity: Gold is a finite resource, making it resistant to devaluation caused by excessive money printing.

- Store of Value: Throughout history, gold has retained its value over time, making it a reliable asset to protect wealth.

- Liquidity: Gold is easily tradable and accepted worldwide, providing investors with a liquid asset during times of economic turmoil.

Relationship with Inflation Rates

The price of gold is often influenced by inflation rates, with higher inflation leading to an increase in demand for gold as a safe haven asset. When inflation erodes the value of paper currency, investors turn to gold as a store of value that can maintain its purchasing power over time.

Income Funds

Income funds are investment vehicles that focus on generating regular income for investors through various sources such as dividends, interest payments, and other fixed income securities. These funds are designed to provide a steady stream of income while also offering the potential for capital appreciation.

Overview of Income Funds

Income funds typically invest in assets like bonds, preferred stocks, real estate investment trusts (REITs), and dividend-paying stocks. These assets are chosen for their ability to generate consistent income, which is then distributed to investors in the form of dividends or interest payments.

- Income funds provide investors with a source of regular income, making them an attractive option for those seeking stable returns.

- These funds often have a lower risk profile compared to growth-oriented investments, as the focus is on income generation rather than capital appreciation.

- Income funds are managed by professional fund managers who allocate the portfolio to maximize income while maintaining an acceptable level of risk.

Risk-Return Profile of Income Funds

Income funds typically offer a more conservative risk-return profile compared to growth-oriented investments like equity funds. While income funds may provide lower potential for capital gains, they are favored by investors looking for steady income and lower volatility in their portfolios.

- Income funds are considered a more defensive investment option, as they are less susceptible to market fluctuations compared to growth investments.

- Investors in income funds are exposed to interest rate risk, credit risk, and reinvestment risk, which can impact the overall returns of the fund.

- Despite the lower potential for capital appreciation, income funds can provide a reliable source of income even in volatile market conditions.

Role of Income Funds in a Diversified Investment Portfolio

Income funds play a crucial role in a diversified investment portfolio by providing stability and regular income to offset the volatility of other investments. By including income funds in a portfolio, investors can achieve a balanced mix of growth and income-generating assets, reducing overall risk while still aiming for long-term returns.

- Income funds help diversify a portfolio by adding assets that are not correlated with traditional equity investments, providing a cushion against market downturns.

- Investors can use income funds to create a reliable income stream for retirement or other financial goals, ensuring a steady cash flow over time.

- By combining income funds with growth-oriented investments, investors can achieve a well-rounded portfolio that balances income generation and capital appreciation.

Index Funds

Index funds are a type of mutual fund or exchange-traded fund (ETF) that aims to replicate the performance of a specific market index, such as the S&P 500. Unlike actively managed funds, which rely on professional portfolio managers to make investment decisions, index funds simply track the performance of the underlying index.

Benefits of Investing in Index Funds

Investing in index funds offers several advantages for long-term investors:

- Diversification: Index funds provide exposure to a wide range of stocks or bonds, reducing individual stock risk.

- Low Costs: Index funds typically have lower expense ratios compared to actively managed funds, making them a cost-effective investment option.

- Consistent Performance: Over the long term, index funds have historically outperformed many actively managed funds due to their low costs and passive investment approach.

- Transparency: Since index funds aim to replicate the performance of a specific index, investors know exactly what they are investing in and can easily track the fund’s performance.

Performance of Index Funds vs. Actively Managed Funds

When comparing the performance of index funds with actively managed funds in various market conditions, index funds have shown consistent results:

| Market Condition | Index Funds | Actively Managed Funds |

|---|---|---|

| Bull Market | Index funds have generally performed well, capturing the overall market gains. | Actively managed funds may outperform in certain sectors but tend to have higher costs and lower overall returns. |

| Bear Market | Index funds have shown resilience during bear markets, minimizing losses due to their diversified nature. | Actively managed funds may struggle to outperform the market and suffer significant losses. |

| Volatility | Index funds provide stability and are less prone to market fluctuations compared to actively managed funds. | Actively managed funds may take advantage of volatility but also carry higher risks. |

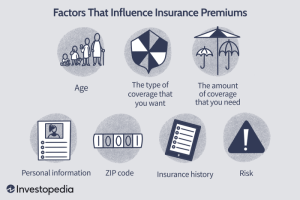

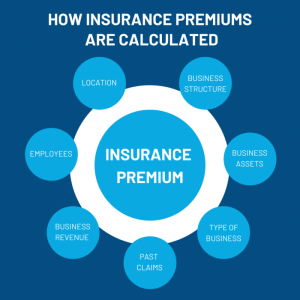

Insurance Premiums

Insurance premiums are the amount of money an individual or business pays to an insurance company to purchase an insurance policy. These premiums are typically paid on a regular basis, such as monthly or annually, to maintain coverage for various risks or liabilities.

Calculation of Insurance Premiums

Insurance companies use a variety of factors to calculate insurance premiums, including but not limited to:

- The type of insurance coverage being purchased

- The amount of coverage needed

- The individual’s or business’s risk profile

- The location of the insured property

- The individual’s age, gender, and health status (for health insurance)

Factors Influencing Insurance Premiums

- Insurance companies consider the level of risk associated with providing coverage to an individual or business. The higher the risk, the higher the premium.

- The type and amount of coverage needed will also impact the cost of insurance premiums. More comprehensive coverage often comes with a higher price tag.

- Demographic factors such as age, gender, and location can influence insurance premiums. For example, younger individuals may pay higher premiums for life insurance.

- Claim history and credit score can also play a role in determining insurance premiums. Individuals with a history of making claims may face higher premiums.

Tips to Lower Insurance Premiums

- Consider bundling insurance policies with the same provider to receive discounts on premiums.

- Opt for a higher deductible, which can lower your premiums but also means you’ll pay more out of pocket in the event of a claim.

- Improve your credit score, as a higher score can lead to lower insurance premiums.

- Review your coverage regularly to ensure you’re not overpaying for coverage you no longer need.

- Ask about available discounts, such as those for safe driving or home security measures.

In conclusion, gold shines as a reliable safeguard against inflation, offering investors a secure haven in turbulent financial climates.

Answers to Common Questions

How does gold perform during high inflation?

Gold tends to retain its value and even increase in price during times of high inflation, making it a popular hedge against economic uncertainty.

What factors make gold a preferred choice as an inflation hedge?

Gold’s intrinsic value, limited supply, and universal acceptance contribute to its appeal as a reliable store of wealth during inflationary periods.

Is there a correlation between inflation rates and the price of gold?

Yes, typically gold prices rise in response to inflation as investors seek assets that can maintain their value in the face of currency devaluation.